Statistical Jump Model#

import matplotlib.pyplot as plt

plt.style.use('seaborn-v0_8-talk')

import numpy as np

import quantbullet.research.jump_model as jm

from quantbullet import set_package_log_level, set_figsize

set_package_log_level('info')

Implementation and API of the model are all at quantbullet.research.jump_model.

Discrete Jump Model: Basic Tutorial#

Default parameters can be loaded using TestingParams class. This loads the same simulation inputs as the related literature. The transition matrix controls the probability of transitioning from one state to another, and the normal distribution parameters control the mean and standard deviation for each state.

transition_matrix, norm_params = jm.TestingUtils().daily()

print(transition_matrix)

print(norm_params)

[[0.99788413 0.00211587]

[0.01198743 0.98801257]]

{0: (0.000615, 0.007759155881924271), 1: (-0.000785, 0.017396608864948364)}

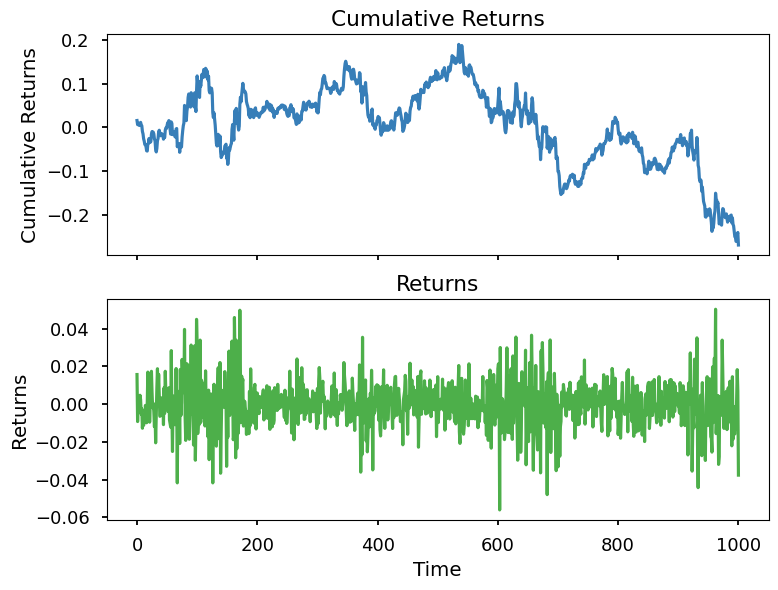

The SimulationGenerator class runs the simulation by first generating the hidden states, then conditional normal returns.

Here, we observed that simulated returns indeed show pattern of volatility clustering.

np.random.seed(999)

sim_states, sim_returns = jm.SimulationGenerator().run(

steps=1000, transition_matrix=transition_matrix, norm_params=norm_params

)

jm.TestingUtils().plot_returns(sim_returns)

10-06 17:42:40 INFO Step 1: Initial (stationary) distribution: [0.84997341 0.15002659]

10-06 17:42:40 INFO Step 2: Simulated states: Counter({0: 633, 1: 368})

10-06 17:42:40 INFO Step 3: Generate simulated return data conditional on states.

To fit the model, FeatureGenerator class enriches the features by adding a family of lagged returns and volatility features. It also standardizes the features.

enriched_returns = jm.FeatureGenerator().enrich_features(sim_returns)

enriched_returns = jm.FeatureGenerator().standarize_features(enriched_returns)

enriched_returns.shape

(988, 15)

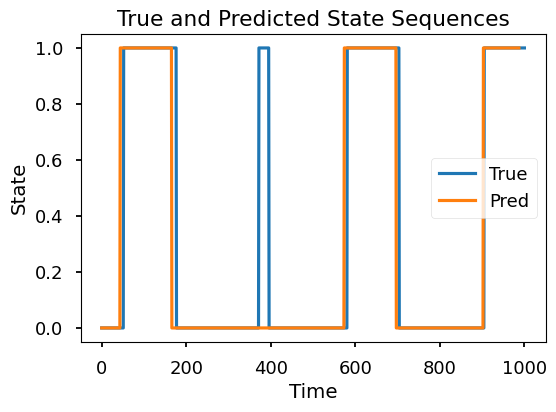

Finally, the dicrete jump model is fitted using DiscreteJumpModel class. Lambda is the penalty parameter for the jumps. n_trials is the number of trials for different initializations, as the algorithm cannot guarantee to find the global optimum. As the result shows, the model is able to uncover the simulated hidden states, except for one short period.

model = jm.DiscreteJumpModel()

res = model.fit(enriched_returns, k=2, lambda_=100, rearrange=True, n_trials=4)

with set_figsize(6, 4):

bac = model.evaluate(sim_states, res['best_state_sequence'], plot=True)

print(bac)

10-06 17:42:44 INFO Mean and Volatility by inferred states:

{0: (0.028637970131994296, 0.7088256592365949), 1: (-0.05710237680864317, 1.4096882064420155)}

{'BAC': 0.9310483870967742}

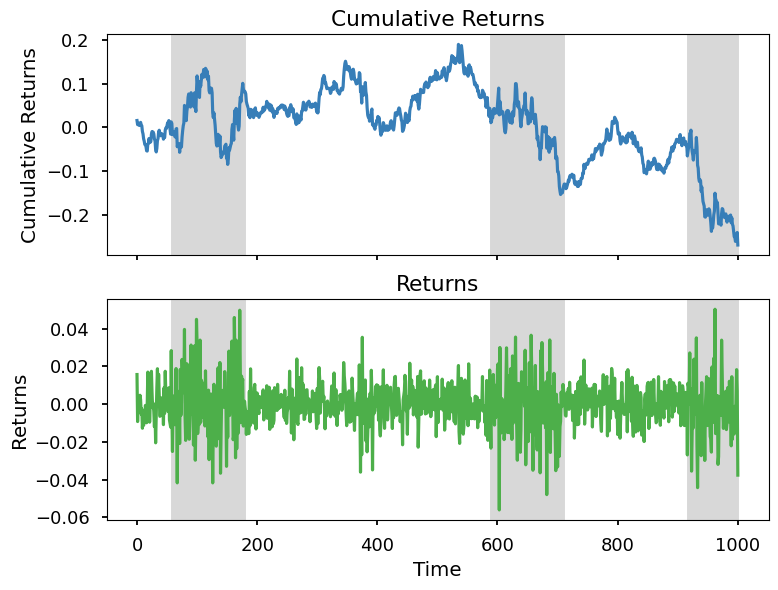

We label the identified states and plot against the returns. The model indeed captures some market downturns.

jm.TestingUtils().plot_returns(np.array(sim_returns), res['best_state_sequence'])

Find the best Penalty parameter#

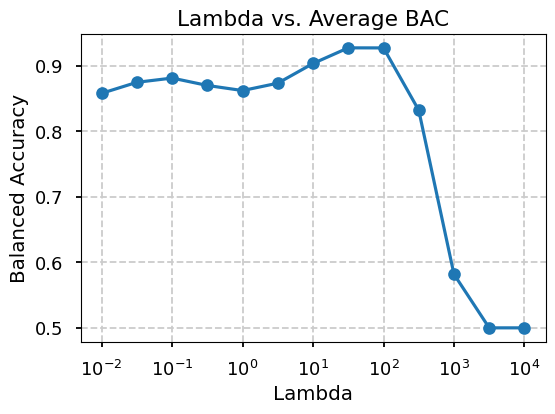

In this section, we aim to find the best penalty parameter for the model. For each penalty parameter, we simulated 50 sequences of states with length 1000, and model runs 8 trials for each sequence. Finally, the average Balanced Accuracy is calculated for each penalty parameter.

from collections import defaultdict

from tqdm import tqdm

import json

bac_lambda_hist = defaultdict(list)

lambda_range = np.logspace(-2, 4, num=13, base=10)

transition_matrix, norm_params = jm.TestingUtils().daily()

model = jm.DiscreteJumpModel()

# for lambda_ in lambda_range:

# for _ in tqdm(range(50)):

# sim_states, sim_returns = jm.SimulationGenerator().run(steps=1000, transition_matrix=transition_matrix, norm_params=norm_params)

# enriched_returns = jm.FeatureGenerator().enrich_features(sim_returns)

# enriched_returns = jm.FeatureGenerator().standarize_features(enriched_returns)

# res = model.fit(enriched_returns, k=2, lambda_=lambda_, rearrange=True, n_trials=8)

# score = model.evaluate(sim_states, res['best_state_sequence'], plot=False)

# bac_lambda_hist[str(lambda_)].append(score["BAC"])

Below results are inline with the best penalty parameter found in the related literature.

bac_lambda_hist = json.load(open('bac_lambda_hist.json', 'r'))

with set_figsize(6, 4):

jm.TestingUtils().plot_averages(bac_lambda_hist)

Continuous Jump Model#

The continuous version of the jump model follows roughly the same procedure as the discrete version, but estimates a sequence of state probabilities instead of a discrete state. The algorithm is generally slower.

Here, we fit the model using the same simulated data and penalty parameter. Without bothering with many initializations and trials, we fit the model until no improvement is observed.

ctsJump = jm.ContinuousJumpModel()

centroids = ctsJump.initialize_kmeans_plusplus(enriched_returns, k=2)

cur_s = ctsJump.classify_data_to_states(enriched_returns, centroids)

second_col = 1 - cur_s

cur_s = np.column_stack((cur_s, second_col))

tol = 100

max_iter = 100

cur_loss = float('inf')

best_states = cur_s

best_loss = cur_loss

no_improvement_counter = 0 # Counter for consecutive iterations without improvement

for _ in range(max_iter):

cur_theta = ctsJump.fixed_states_optimize(enriched_returns, cur_s, k=2) # Assuming 2 states

lossMatrix = ctsJump.generate_loss_matrix(enriched_returns, cur_theta)

C = ctsJump.generate_C(k=2)

cur_s, cur_loss = ctsJump.fixed_theta_optimize(lossMatrix, lambda_=100, C=C)

# Check if the current solution is better than the best known solution

if cur_loss < best_loss:

best_loss = cur_loss

best_states = cur_s

no_improvement_counter = 0 # Reset the counter if there's improvement

else:

no_improvement_counter += 1 # Increment the counter if no improvement

# Check for convergence

if no_improvement_counter >= 3:

break

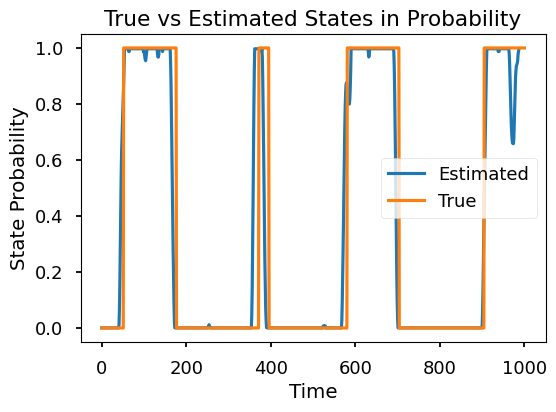

The model is shown to be more dynamic, and indeed captures the pattern we didn’t see in the discrete version.

with set_figsize(6, 4):

plt.plot(cur_s[:, 0], label='Estimated')

plt.plot(sim_states, label='True')

plt.title('True vs Estimated States in Probability')

plt.xlabel('Time')

plt.ylabel('State Probability')

plt.legend()

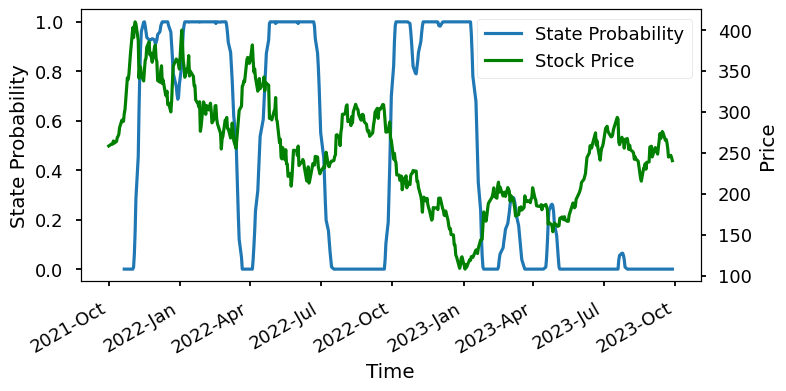

Working with Real Data#

To work with real data, we also use the daily returns of a stock, and fit the model using $\lambda=100$ as we have found to be the best in the simulation testing. For other frequencies, the model needs to be re-calibrated to find the best penalty parameter.

import yfinance as yf

# Define the ticker symbol

ticker_symbol = "TSLA"

# Fetch data

data = yf.download(ticker_symbol, interval="1d", period="500d")

[*********************100%%**********************] 1 of 1 completed

log_ret = np.log(data['Adj Close'] / data['Adj Close'].shift(1)).dropna().values

enriched_returns = jm.FeatureGenerator().enrich_features(log_ret)

enriched_returns = jm.FeatureGenerator().standarize_features(enriched_returns)

ctsJump = jm.ContinuousJumpModel()

best_states, best_loss = ctsJump.fit(enriched_returns, k=2, lambda_=100, n_trials=10)

Model strikes a good balance between dynamics and persistence. Almost all market downturns are captured, and the probability transitions are smooth.

with set_figsize(8, 4):

# Two states maybe flipped, so we need to rearrange them

jm.TestingUtils().plot_state_probs(best_states[:, [1, 0]], data['Adj Close'])